Fertiliser shortage due to Iran war may threaten next year’s grain harvests

Farmers are in a worse situation than during the 2022 fertiliser crisis. Analysts warn of lower yields and reduced planting areas as ongoing conflict disrupts markets.

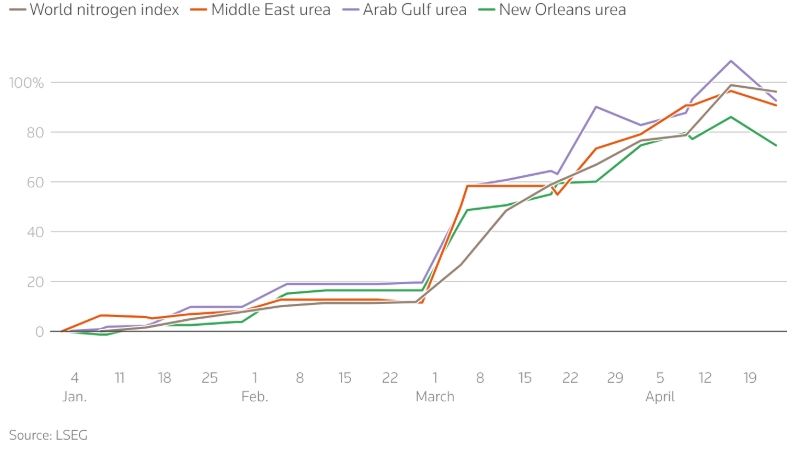

Dynamics of urea prices in different regions

Farmers worldwide are facing a second sharp rise in fertiliser prices in four years due to the Iran war. With grain prices too low to offset the deeper supply squeeze this time, many are reconsidering planting plans, putting global food production at risk.

The Middle East is a key fertiliser production hub, and much of global trade passes through the Strait of Hormuz, where shipping has been severely disrupted by the conflict.

Supplies of urea — a nitrogen fertiliser — from the world’s largest facility in Qatar have been halted, while flows of sulphur and ammonia have also been constrained.

With no quick resolution in sight, analysts and industry players fear the situation could become even worse than in 2022. According to Shawn Arita of North Dakota State University, the current supply squeeze is significantly more severe.

Since the start of the war, fertiliser prices have surged, especially urea, reflecting the loss of roughly one-third of global exports from the Gulf region.

Some countries continue to buy: India has secured record volumes of urea, paying nearly double compared to two months ago. However, such prices are unaffordable for many farmers.

Unlike in 2022, lower grain prices now fail to offset rising costs. Chicago wheat prices are about half their level of four years ago, while soybean prices are nearly 50% lower.

As a result, many farmers lack the income needed to cover fertiliser costs.

Nitrogen fertilisers are essential for yields and quality, including protein levels in wheat. Farmers may cut back on phosphate and potash use, but even these markets could tighten due to export restrictions and supply disruptions.

Some producers may ultimately reduce fertiliser application, putting yields at risk.

At least 2 million tonnes of urea production (around 3% of global seaborne trade) have been lost since the conflict began, while nearly 1 million tonnes remain stranded in the Gulf.

Even if the Strait of Hormuz reopens soon, clearing the backlog will take weeks, and supply constraints could persist for months.

Although stocks remain relatively high after strong harvests last year, organisations are already lowering crop forecasts. The United Nations has warned of food security risks, especially in developing countries.

The situation could mirror 2022, when high fertiliser prices worsened hunger, particularly in East Africa.

In Australia, wheat planting area is expected to fall by 14% as farmers shift away from fertiliser-intensive crops. Similar trends may emerge elsewhere.

In Brazil, farmers may reduce fertiliser use or switch to cheaper alternatives, while palm oil yields in Southeast Asia could also decline.

In Europe, planting decisions are shifting away from corn, and reduced nitrogen use may lower wheat quality.

The biggest risk lies ahead in the autumn planting season, when financially strained farmers may cut overall grain area.

Analysts are already expressing concern about the 2027 harvest.

Read also

Ukraine initiates urgent UN Security Council meeting on shipping safety in the Bla...

Jordan cancels barley tender and issues a new one

UkrAgroConsult Advises on In-House Power Generation Projects

Russian attacks on Ukraine’s ports increase logistics costs and put pressure...

Global lentil market remains stable as Canadian crop prospects improve

Got additional questions?

We will be happy to assist!

Write to us

Our manager will contact you soon