Sector Of The Year: The ‘golden crop’ shines bright on external factors but ends the year almost unchanged

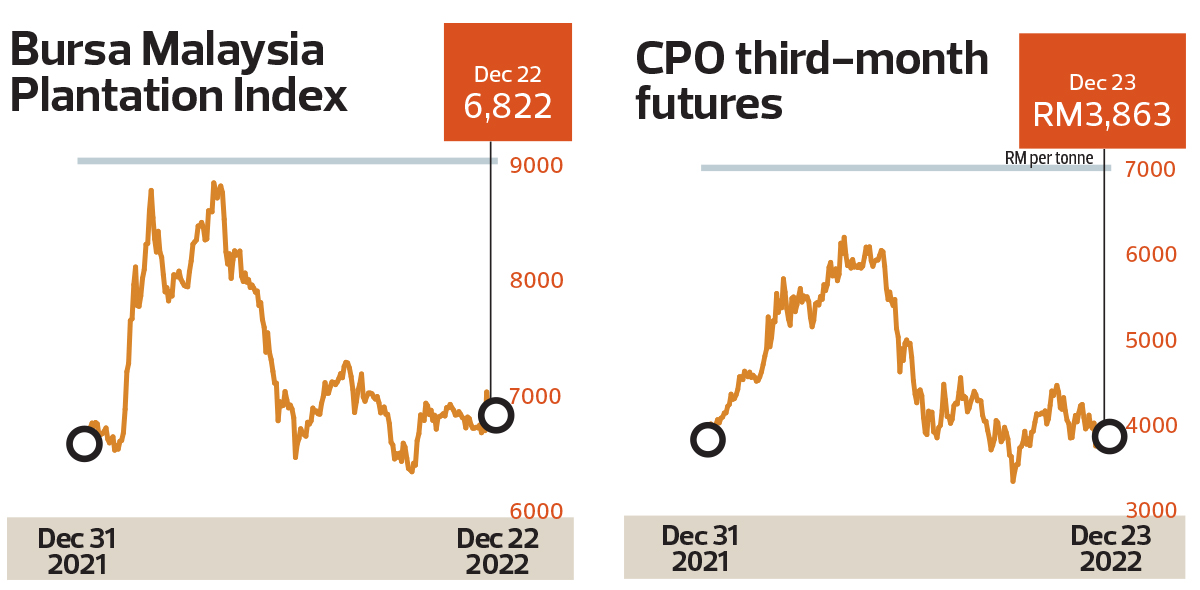

Like many other commodities, Malaysia’s golden crop — palm oil — went through a whirlwind of a year. The upward trend in prices saw interest return to plantation counters that had missed out on the rally in crude palm oil (CPO) prices in 2021.

The CPO spot month futures hit a high, surpassing RM8,000 per tonne, following news that Russia had launched an attack on Ukraine. Prices were also supported by the intense labour shortage in oil palm plantations, owing to Covid-19-related disruptions, but regulatory policies and softening demand from China, as a result of Beijing’s zero-Covid policy, weighed on the commodity later.

The Black Sea region conflict between Russia and Ukraine contributed significantly to the increase in CPO prices, which set new records in February this year, surpassing the highest price registered in 2008.

“This is an important factor that drove prices for Malaysia to an all-time high,” says Phillip Futures Sdn Bhd derivative products specialist David Ng.

Palm oil was sought after as buyers rushed to secure replacement stocks for sunflower oil shipments, which were disrupted by Russia’s invasion of Ukraine. According to the Observatory of Economic Complexity, Ukraine accounts for the largest exports of sunflower products in the world, supplying some 46% of sunflower-seed and safflower oil production while Russia exports 23% of the global supply.

“You will have to look at palm and related oils because Ukraine and Russia together are exporters of sunflower oil. Whenever Russia refuses to renew their deal (the UN-brokered grain deal), then we can see basically palm oil prices going up because of the concern of shortage in sunflower oil,” says Sathia Varqa, co-founder of Singapore-based Palm Oil Analytics.

India — the largest importer of sunflower oil from the Black Sea region — has also shifted some of its demand to Malaysian palm oil, owing to uncertainty in sunflower oil supply. “This clearly boosted CPO prices in Malaysia,” he explains.

Sathia adds that buyers also took advantage of the widening discount between palm oil and rival soybean oil, which rose to almost US$800 per tonne — historically above the average spread of US$100 to US$150 per tonne — further adding to the price surge in CPO.

As the price of cooking oil refined from CPO rose in the domestic market, Indonesia — the world’s largest producer of palm oil — imposed a ban on the export of the commodity and its derivatives on April 28. The move pushed CPO prices even higher.

Less than one month later, however, the Indonesian government reversed the ban, following protests from smallholders who have had to accept lower prices from millers for their fresh fruit bunches (FFB) as tankers were still full because of the ban on exports.

The lifting of the ban — to flush out high inventory levels in Indonesia — sent CPO prices lower.

In Malaysia, the fall in CPO prices caused palm oil millers to stop buying FFB as the buying price, based on the monthly average, remained high but the selling price for the extracted oil, based on the daily market price, had fallen. This prompted the Malaysian Palm Oil Board (MPOB) to warn millers in late June to continue buying FFB or have their licences revoked.

CPO prices halved by mid-July, owing mainly to Indonesia’s flip-flopping on its export policy. Worries over a global recession added to the short-lived rally in CPO prices. At the time of writing, the CPO third-month contract was trading at RM3,875 per tonne, down 47% from its peak of more than RM7,000.

The surge in CPO prices in March saw investors rushing into plantation stocks on Bursa Malaysia. The stocks had been unloved for some time because of environmental, social and governance (ESG) concerns.

“Plantation stocks rallied in the early part of this year, attributed mainly to the all-time high prices of CPO as a result of the Ukraine and Russia conflict. It was further aggravated by the CPO export ban by the Indonesian government, which prompted a major demand shift over to the Malaysia CPO market,” says Ng.

Shares in selected plantation companies surged this year in response to three major events that significantly influenced the edible oil market — the Ukraine war, Indonesia’s blanket ban on exports and its reversal on May 23.

Kuala Lumpur Kepong Bhd’s (KLK) share price in the February-to-May period surged 4.02%, with the highest price recorded on April 29 at RM29.17. On a year-to-Dec 22 basis, the stock rose only 1.14% to RM21.26.

Genting Plantations Bhd shares fell 3.45% in the February-to-May period despite posting the highest share price of RM9.16 on March 3. Genting Plantations’ shares have shed 5.78% year to date (YTD) to RM6.04.

IOI Corp Bhd fell 5.49% during the February-to-May period, with the peak share price recorded on April 25 at RM4.63. YTD, the counter added 3.51% to RM3.94.

Sime Darby Plantation Bhd’s shares rose 10.56% in the said period with the highest share price recorded on May 5 at RM5.14. YTD, the counter has risen 22.65% to RM4.40.

Meanwhile, United Plantations Bhd saw its share price rise 6.12% during the period, with the highest price recorded on April 26 at RM15.59. YTD, its shares have gained 17.87% to RM15.18.

The ongoing labour shortage — which began when Covid-19-related border closures choked off the supply of migrant workers to plantations in Malaysia — is still the biggest concern among planters.

According to the MPOB, in August this year, the oil palm plantation sector’s total labour requirement was 437,212. The number of workers in the sector was only 382,582, however, for a shortage of 54,630 workers.

The shortage of labour left fruit unharvested on palm oil trees, causing producers to miss out on billions of ringgit in the form of lost revenue.

The Malaysian Palm Oil Association (MPOA) estimated RM20 billion in revenue losses for the sector and said the foreign workers approved for the sector translated into only 19% of the total required in 2022.

Apart from the severe labour shortage issues, producers were further punished by the Withhold Release Orders (WRO) imposed by US Customs and Border Protection. Two listed plantation companies — Sime Darby Plantation Bhd and FGV Holdings Bhd — were slapped with WROs for findings of forced labour in their plantations and alleged human rights violations in 2020. Both companies are still working towards resolving the WRO.

These issues played out in the bigger theme of ESG investing, where Malaysian palm oil producers were panned by investors who had made ESG a core part of their investment process.

“ESG concerns are definitely an ongoing issue despite the fact that a lot of Malaysian producers already adopted sustainability certificates such as the Roundtable on Sustainable Palm Oil (RSPO) and Malaysian Sustainable Palm Oil (MSPO). But this is going to be a mid-term issue and will always be on investors’ minds,” says Ng.

Pressure has also been mounting from the European Commission’s proposed regulation for deforestation-free products, which is aimed at minimising the degradation of forests globally. According to the proposed regulation, six commodities — palm oil, beef, wood, soybeans, cocoa and coffee and their derivative products, which were grown or raised on land that was subjected to deforestation or forest degradation — will be banned from entering the European Union after the regulation is passed by the Council of the EU.

The strict zero-Covid policy in China, which is a major importer of Malaysian palm oil, has weighed on CPO demand. According to MPOB data, Malaysia’s exports to China during the first half of the year have already nosedived 24% year on year.

From the January-to-November 2022 period, Malaysian palm oil exports to China were down 30% y-o-y, says Sathia.

“So, that has been one of the reasons for soaring stocks in Malaysia. If you look at the MPOB numbers, the stocks have been holding at about two million tonnes since August this year. That is quite high. In November, the inventory had risen to 2.8 million tonnes, which is higher than usual,” he tells The Edge.

According RHB Investment Bank Bhd analyst Hoe Lee Leng, however, China has been restocking from Malaysia, buying 36% more palm products month on month (m-o-m) in October, which resulted in its stock levels rising to 6% above historical levels (versus -19% in September).

“India started buying more from Malaysia again, as evidenced by the 13% m-o-m rise in imports from Malaysia. Still, it may have reduced buying from Indonesia, as its palm oil stock levels fell back to 14.5% below historical levels in October (from 5% below in September),” she says in a research note.

China’s toughest zero-Covid policy has collapsed demand for commodities, including palm oil. The country has since early this month eased some of the restrictions under the policy despite the soaring number of Covid cases.

Indonesia — which is very likely to kick-start its biodiesel mandate, known as “B35”, from January 2023 — could be a strong boost for CPO price next year, says Sathia.

“This means greater absorption of CPO in Indonesia will happen to cater for its domestic market B35 mandate. We expect about 12 million tonnes of CPO to be used to meet the B35 biodiesel demand. This also means Indonesia will have a smaller supply for the export market, causing more international buyers such as India to depend on Malaysia for their supply of CPO,” he adds.

Currently, Indonesia uses B30 biodiesel, which contains 30% palm oil. He adds that although this may greatly support Malaysia CPO prices, such a big demand may not be good news for Malaysian refineries that rely on CPO to produce olein, stearin and fatty acids.

“With all CPO going out of the country, where would they [refineries] find CPO? Malaysian refineries usually buy CPO from Indonesia. You don’t want to be in a market situation where upstream CPO is moving out of the country,” he adds.

He believes China is likely to hold the key to another potential upside to the CPO price next year.

“If China continues to ease its Covid policy, we can expect greater exports from Malaysia and Indonesia going into the country. Usually, there is strong seasonal demand before Chinese New Year. But, at this point, it’s difficult to be too optimistic with China, because they seem to be easing, but Covid cases are surging,” Sathia explains, noting that abrupt shifts in Covid policy in China may not necessarily mean a sustained rise in CPO exports.

“If China comes around, Malaysian stocks will come down very quickly, and the price will shoot up. We can see prices rising to between RM4,500 and RM5,000 per tonne. So, we are quite bullish. The lowest it can go, assuming China further restricts its Covid policy, will be between RM3,600 and RM3,800,” says Sathia.

Read also

Ukraine’s Ministry of Agrarian Policy resumes operations after government re...

Wheat prices in Moldova rise due to logistics disruptions in the Azov and Black Seas

US drought and China’s aggressive buying are pushing up soybean prices

Export logistics problems send wheat prices down at Russian ports

Malaysia to test B100 palm biodiesel on agricultural machinery

Got additional questions?

We will be happy to assist!

Write to us

Our manager will contact you soon