Soybean outlook: South American soybeans poised to reap rewards of Trump’s tariff war

Donald Trump’s return to the US presidency has revived the threat of tariffs as a trade negotiating tactic, bringing widespread disruption to the world economy. For soybeans, the onset of tariffs targeting the US’s number one soybean customer, China, threatens to resume the same stand offs seen in the first Trump administration – although second time round, China is ready, and South America is poised to capitalize.

Global soybean markets have taken much of President Trump’s tariff disturbance in their stride – despite the renewed tension between the primary global buyer and one of its major suppliers. But with production forecasts calling for the 2025/26 marketing year to deliver the largest soybean crop in history – nearly 427 million tonnes according to the USDA’s forecast – decisions made today will have long term consequences. Could US tariffs simply consolidate a trend that has already seen South American production surge and trade ties to China deepen?

From the outset of the new Trump administration, tariffs were clearly back on the agenda. With the arrival of the first full month, February 2025 brought the first signs of the gear shift in US policy – but among the trails of red that marked stock markets and other commodities, front month soybean futures on the Chicago Mercantile Exchange closed just 1% lower at the end of the month. That came despite President Trump announcing a 10% tariff on Chinese goods, and 25% tariffs on Mexico and Canada, all key customers for US agricultural products.

Any deterioration in the state of US-China trade relations would be cushioned by the US being out of its peak soybean export period, while Brazil and Argentina were in the thick of theirs. However, early signs suggested that late demand for old crop US soybeans tailed off, leaving farmers with bigger ending stocks than expected – a dynamic that is likely to signal price pressure as the year goes on.

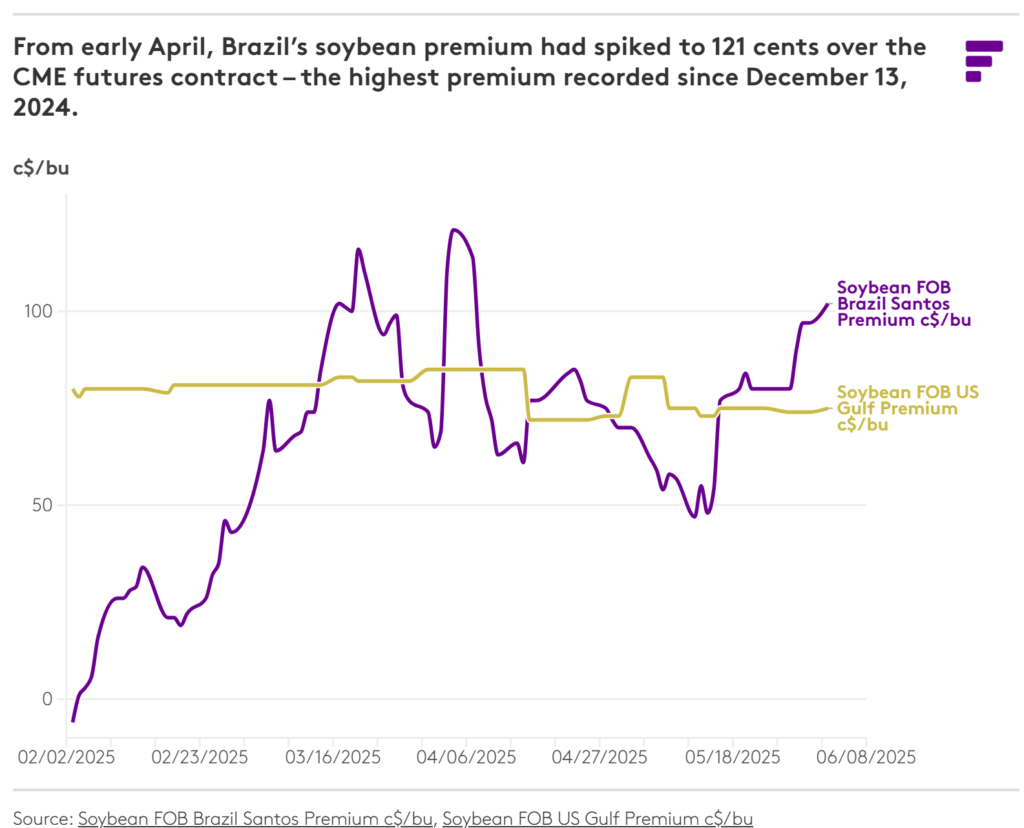

Record-breaking harvests in South America added to the competition as Brazil and Argentina reported favorable weather that bolstered crop yields, but physical prices told a clear story as US Gulf soybean prices fell while Brazilian soybean prices in the key export port of Santos rose steadily.

US Gulf soybean prices started the period at $423 per metric tonne on February 4, a $28.25 per tonne premium to Brazil as South America’s huge 220 million tonne harvest kept prices low.

With the US building barriers to Chinese trade, South America looked set to extend its dominance in Chinese soybean sourcing, while the US faced a growing surplus of unclaimed stock.

March brought heightened activity as trade policies tightened.

With stricter tariffs on US soybeans, China turned almost exclusively toward Brazil and Argentina to fulfil its needs, supporting physical prices in key South American export hubs. That demand saw Brazil’s FOB Santos differentials rise sharply, closing the gap to values seen in the northern rival until by early-March they were just $1.50/t behind US Gulf soybeans.

The shift in buying patterns saw price indications for the US export market dry up, leaving values to flatline for much of the period to date amid a lack of interest. For South America, the trade drove Brazil’s physical pricing differentials sharply above those of the US in a seasonally unusual pattern.

More tellingly, the differential to the CME’s soybean futures contract paid to buy physical cargoes of Brazilian soybeans surged in the January through March period, despite it being the key harvest season when harvest supply usually weighs on values.

Brazilian soybeans loading in Santos were assessed at a 20 cents per bushel discount to the CME’s soybean contract on January 24, 2025, but the mounting interest for the giant crop quickly drove premiums to a 116 cent premium to the futures contract by March 20.

More unusually though, the escalation in trade tensions tripped off buying of Argentine soybeans as China’s state-backed food agency Sinograin stepped in to snap up stocks. Fastmarkets tracked up to 41 Argentine cargoes, equivalent to just over 2.7 million tonnes, while government data shows export licence registrations for nearly 3 million tonnes of beans for shipment during the period.

Argentina typically processes its own soybeans and exports instead of meal and soybean oil, with the 3 million tonnes of soybeans booked for export equating to between half and two-thirds of the country’s typical full-year export figure. That sparked concerns within Argentina that an export rush could starve the country’s huge crush sector. Could that set up the possibility later in the year of US soybeans being imported to Argentina to meet crush demand? That would be uncommon – but not unprecedented – with the US exporting nearly 2 million tonnes of soybeans to Argentina back in 2018, during the previous Trump administration.

By April, the US administration rolled out a 10% baseline tariff on all imported trade, along with further tariffs that varied across each nation, while the US-China tariff situation escalated dramatically. Losing patience, US tariffs on Chinese products soared to 145%, and China retaliated by increasing US import taxes to 125% – levels that effectively closed off all trade between the two superpowers.

For Brazil, the physical premium to buy beans had spiked to 121 cents over the CME futures contract – the highest premium recorded since December 13, 2024. Beneath that, outright prices also recovered as the underlying CME soybean future regained ground as traders anticipated a thaw in US-China rhetoric, and the potential raising of US biodiesel volumes amid rumors of an update to US biofuel policies.

Four months into the new US administration, and global soybean trading appeared to be settling into a new reality. South America’s production capacity set down a new marker, with the USDA revealing its first forecast for 2025/26 soybean production in Brazil, Argentina and Paraguay of 234.5 million tonnes – a 3% increase on the previous year, and some 55% of total world supply.

In export stakes though, the increase is even more pronounced with 66% of export supply expected to come from the three major South American players – a 2 percentage point increase on 2024/25 figures.

That points to a potential pathway for China to largely insult itself from US tariffs through its relationships with Brazil and Argentina, with South America dominating Chinese demand, while the US caters to the rest of the world.

Whether tariffs remain on the table through the latter part of 2025, there are already some clear trends that will likely leave their mark on the second half of the year.

The big story will become clearer as the final quarter of 2025 comes into focus – the post-harvest period that usually sees a spike in US soybean exports to China. If Chinese tariffs on US beans remain, even at the current 23% derived from the 20% retaliatory US tariff hikes and a 3% tax applied to all origins, the net effect would likely drastically increase Brazil’s already dominant market share into China.

Such a move would support expectations of higher physical premiums for Brazilian soybeans, and potentially be bearish for US premiums – which would have a potential knock-on effect for US planting intentions and production estimates, as US farmers switch to potentially more attractive crops, with corn likely to gain planted area as a result.

The US will need to push its soybeans to other markets, such as Mexico, while talks with Pakistan and Vietnam could ease the export path into those areas. Europe could also be another destination, but all will depend on how trade talks between the US and its trade partners – particularly those in the European bloc – evolve.

Another area to watch is the uncertainties around US biofuel policies. A major domestic source of demand could arise if the US government paves the way for crop-based oilseed feedstocks to find a way into the burgeoning demand for renewable diesel and sustainable aviation fuel. However, any signs that the US government is cooling its interest in biofuels could spell disaster for both the US staples of corn and soybeans.

The Trump soybean tariff war has left a mark on agricultural economics. But what should global supply chain heads, traders, and producers expect moving forward?

- 1. Restructuring of trade dependencies

Brazil appears poised to solidify its market dominance by leveraging robust trade agreements with key buyers like China. Meanwhile, US producers may need to shift focus toward adjacent regional partners such as Mexico or explore policies targeting European market penetration over Asian recovery strategies – all of which may prove difficult if retaliatory tariffs are triggered.

- 2. Biofuel demand may yet change the dynamic

Many biofuel mandates and policies have tried to break the ‘food versus fuel’ debate, by incentivizing the use of waste-based feedstocks such as animal fats or used cooking oil. However, with sustainable aviation fuel in particular showing huge potential demand in the future, any relaxation on use of US soybean oil in the renewable energy space could spark substantial demand.

- 3. Evolving risk mitigation practices

From industrial action triggering fluctuating freight timelines to the weather’s influence on yields and output, the role of predictive analytics for tracking future positioning cannot be overstated within commodity management leadership. Pairing that with effective risk management tools, backed by independent, impartial and comprehensive price reporting services means you are better able to see risks before they develop and protect yourself before they hit your profitability.

Further development of the grain and oilseed markets of Ukraine and the Black Sea region will be in the spotlight of the BLACK SEA GRAIN. KYIV conference, taking place on April 22–23 in Kyiv. The event will focus on strategic directions for the agricultural sector through 2030, including investments, energy independence, processing, and exports of high-value products.

Join strategic discussions and networking with industry leaders to gain актуальна insights, discover new business opportunities, and build partnerships with key market players.

Read also

Black Sea & Danube: Crop and Export Forecast

Ukraine to expand sunflower and rapeseed area while soybeans decline — FAS USDA

Wheat faces biggest weekly drop in eight months on higher inventories

Cargill’s head of world trading departs firm after three decades

Indonesia deploys African weevils to boost palm oil output

Got additional questions?

We will be happy to assist!

Write to us

Our manager will contact you soon