Situation on the global wheat market has changed recently, although it is easy to overlook

The global wheat market has changed recently, though it was easy to miss.

World wheat export supplies are not expected to fall to multi-year lows in 2024-25, which was perhaps predictable based on recent trends.

But the relief may be temporary. Poor prospects for the upcoming wheat harvest in Russia and Ukraine, which account for about 30% of global wheat exports, mean that the supply squeeze could return in 2025-26, and perhaps for real this time.

CHANGING PACE

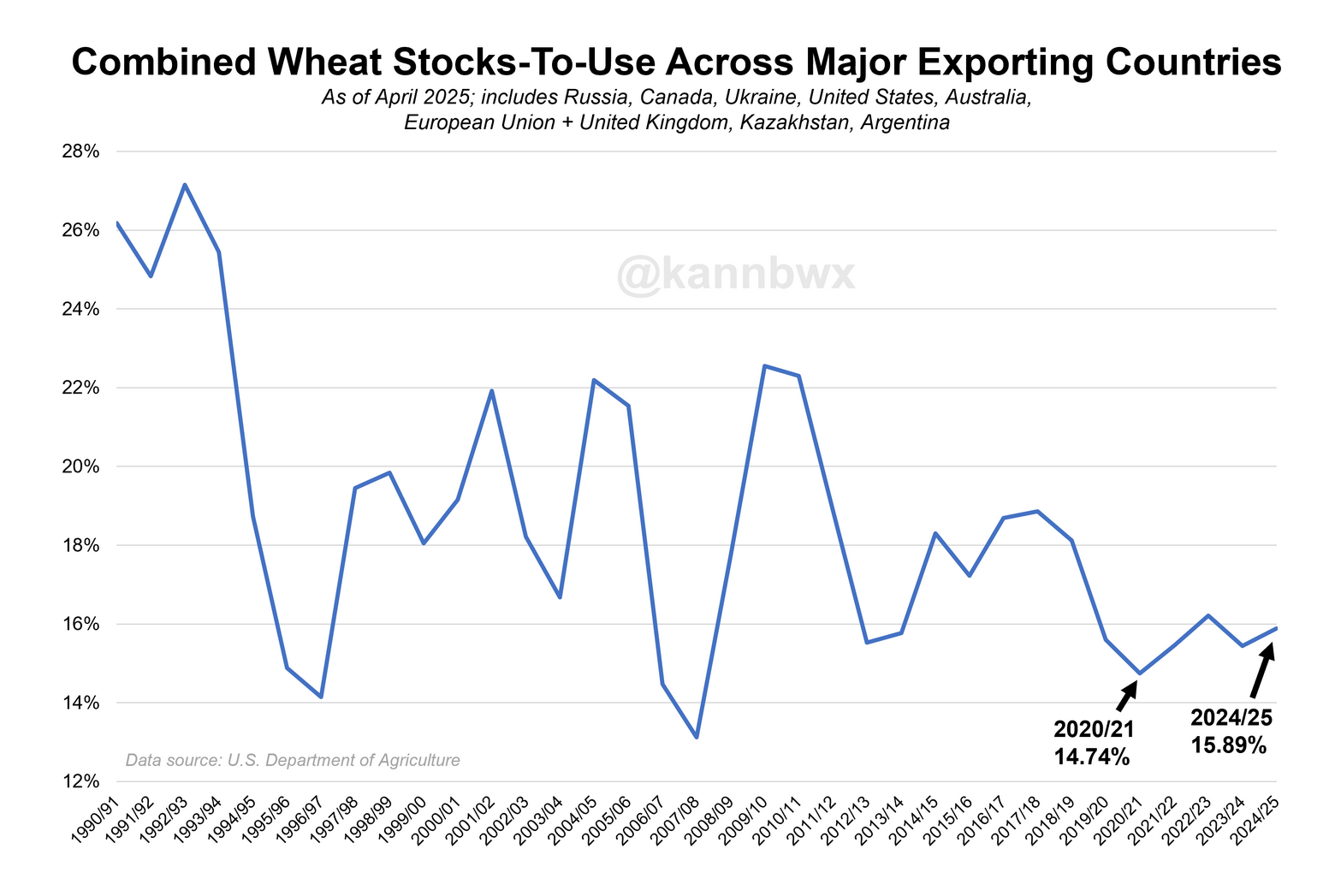

Two months ago, USDA forecasts showed that world wheat stocks-to-use (SU) among major exporting countries would reach a 17-year low of 14.56% in 2024-25.

But this month’s update shows the figure at 15.89%, the second-highest in six years. That’s largely due to sharp declines in China’s wheat import estimates over the past three months.

At the end of the last decade, the average for world wheat production among major exporters was above 18%, so the 2024–25 target is still below the long-term average.

However, the USDA projects that world wheat prices will hit decade-lows each year for at least three years, then gradually rise as marketing years progress.

The 2020–21 SU of 14.74% is currently the lowest since 2007–08, so that’s a number to keep in mind as we move into 2025–26.

Russia and Ukraine

The Kyiv USDA attaché last week estimated the 2025-26 Ukrainian wheat crop at 17.9 million tons, a 13-year low and down 23% from last year. Soils were extremely dry at planting time and profitability is low, leading to a reduction in planted area.

Russian agencies are now forecasting the 2025-26 crop in the range of 79.7 million to 82.5 million tons, comparable to last year’s total.

Favorable weather here could boost yields in both countries and allay concerns, but the early numbers are worth a downgrade, especially since the attaché predicts Ukraine’s 2025-26 wheat exports will be less than half of their record volume.

Russian food and fertilizer exports are not subject to direct Western sanctions, but Moscow says measures against Russian companies involved in these shipments should be lifted.

A bumper harvest has allowed Russian wheat exporters to record their highest volumes in the 2022-23 and 2023-24 marketing years.

A smaller wheat harvest in Russia last year will push wheat exports in 2024-25 to a three-year low, but the share of the exported crop will remain high because Russian grain prices are significantly lower than those of competitors.

Possible talks on a potential ceasefire between Russia and Ukraine will not significantly affect the forecast for wheat production in 2025-26, as most of the crop has already been planted.

DON’T FORGET

U.S. wheat acreage in 2025-26 is set to fall 1.6% from a year ago, including a 55-year low for the high-protein spring variety. U.S. winter wheat was in slightly worse shape as of Sunday than it was a year ago.

Argentina’s 2025-26 wheat crop could be a record if a temporary export tax cut is extended beyond June, making it more attractive to farmers.

Farmers in Canada are planning to increase wheat acreage in 2025-26, while drought in parts of Australia could cut the upcoming harvest by 16% from last year. In the European Union, soft wheat yields are expected to rise 8% from a year ago.

Argentina, Australia, Canada, the European Union and the United States together account for about 54% of global wheat exports, so they also deserve attention on May 12, when the U.S. Department of Agriculture releases its initial forecasts for 2025-26.

Karen Brown is a Reuters market analyst. The views expressed above are her own.

Read also

Kenya expands oilseed farming to reduce dependence on imports

Ship carrying stolen Ukrainian grain denied unloading in Turkey after rejection in...

Germany expected to see lower wheat harvest in 2026

Corn sowing is nearing completion in France

Iran is discussing with Oman the creation of a permanent toll for passage through ...

Got additional questions?

We will be happy to assist!

Write to us

Our manager will contact you soon