Increased pork demand raises US hog prices

The pace of US hog slaughter was higher than expected in February as processors bid up hog prices in response to wholesalers’ increased demand for pork, according to the most recent USDA Livestock, Dairy and Poultry Outlook report.

February ended with estimated federally inspected (FI) hog slaughter numbers just shy of 11 million head, almost 5% higher than a year ago after accounting for the month’s extra slaughter day.

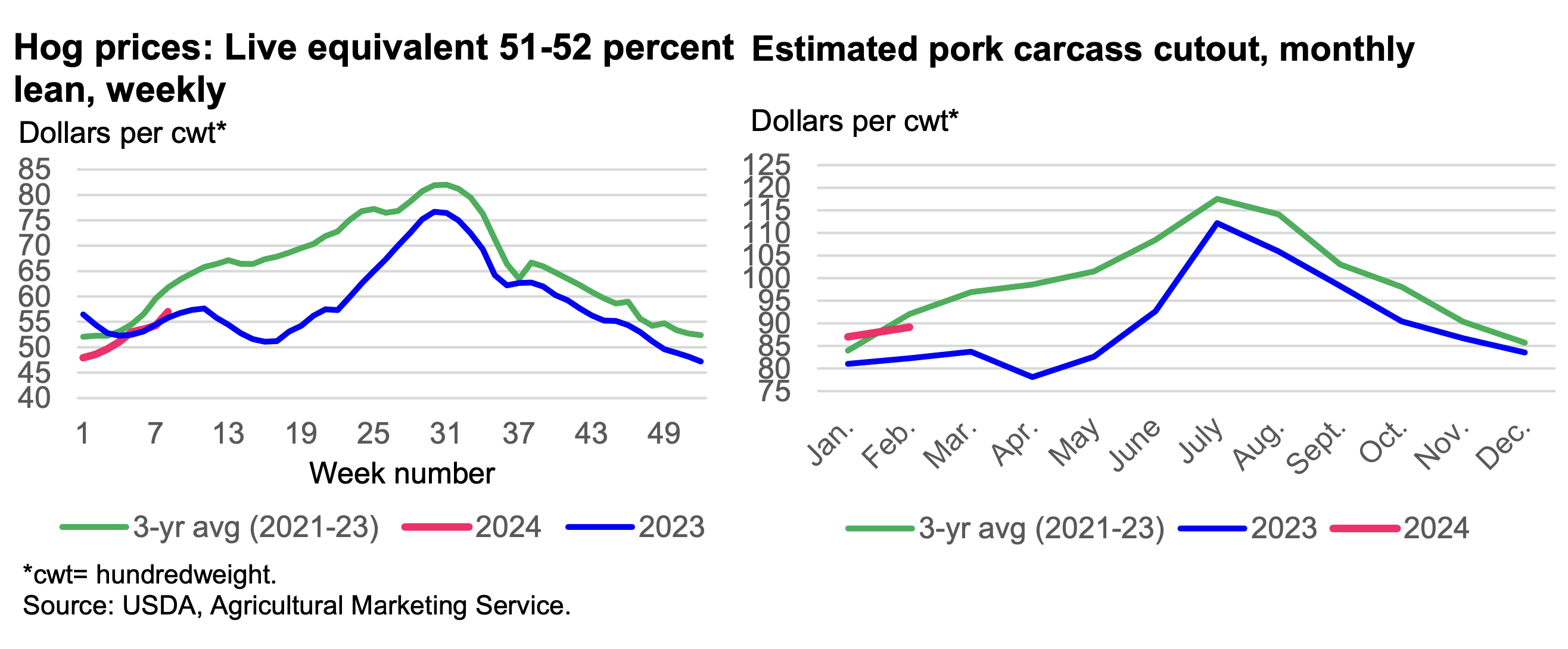

The February live equivalent price of 51–52% lean hogs averaged $55.24 per cwt, 1.8% higher than a year ago. Similarly, processors and wholesalers sold about 2.4 billion pounds of pork—almost 5% more than in February 2023—at estimated pork carcass cutout values of $89.14 per cwt, 8.3 percent higher than a year ago. Increased wholesale demand—higher volumes of pork sold at higher prices—likely provided sufficient margin for processors to pay higher prices for larger numbers of hogs.

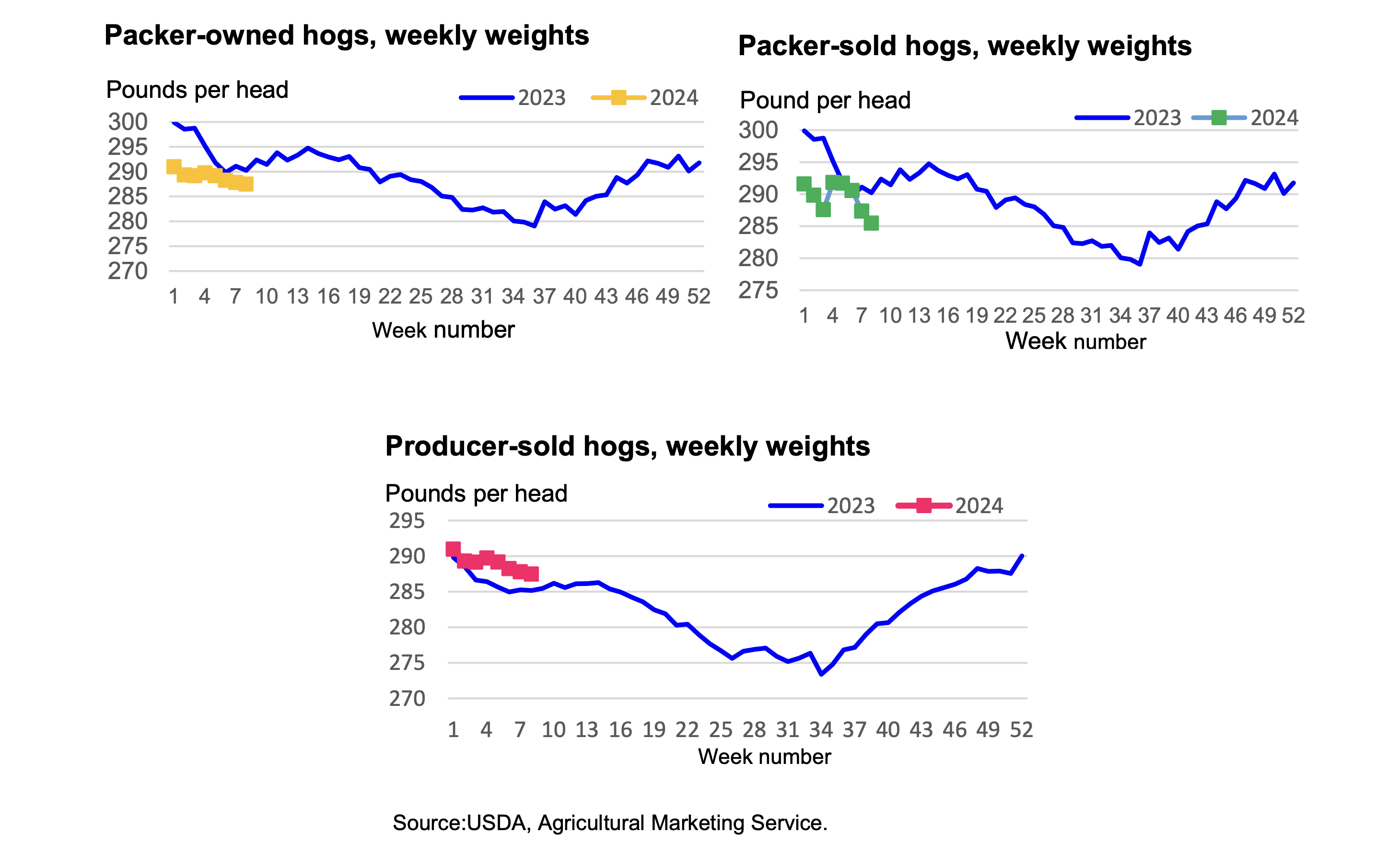

First-quarter pork production is raised about 30 million pounds to almost 7.2 billion pounds, 1.3 percent greater than a year ago. It is likely that some of the hogs supplying the additional production were packer-sold and packer-owned hogs, whose lower than year-earlier weights─despite lower feed costs this year—suggest that they were pulled forward in response to increased pork demand. It is notable that producer-owned hog weights this year are, so far, above year-ago levels, suggesting an unanticipated run-up in wholesale demand by processors.

Demand for hogs in 2024 is expected to be maintained by continued strength in pork demand. Carcass cutout values for January and February suggest that while not likely to achieve 2021–22 levels, values should trend above those of 2023. Wholesale pork demand is expected to be supported by high relative retail prices of pork substitutes, generally high grocery prices in become less of a presence, particularly in Asian markets due to lower EU pork production and higher prices.

First-quarter prices of 51–52% live equivalent lean hogs are expected to average $55 per cwt, about equal to the same period last year.

Second-quarter prices are raised to $65 per cwt, almost 15% above the same period last year.

Third-quarter hog prices are raised $1 from last month’s forecast to $67 per cwt, more than 3% lower than the third quarter of 2023.

The fourth-quarter forecast remains $56 per cwt, almost 5% greater than a year earlier. The revised forecasts average to $61, almost 4% higher than the average for 2023.

Read also

Poland Rapeseed Market Enters a Phase of Feedstock Deficit and Rising Competition

UK scientists develop soy traceability tool to combat deforestation

Truce did not calm the markets: Strait of Hormuz is almost blocked, crude oil pric...

Black Sea & Danube: Crop and Export Forecast

USDA analysts left unchanged the forecast of corn exports from Ukraine

Got additional questions?

We will be happy to assist!

Write to us

Our manager will contact you soon