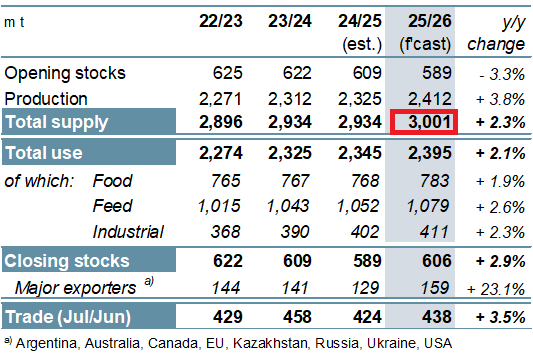

For the first time in history, the total volume of grain on the market will exceed 3 bln tons – IGC

Led by upward revisions for wheat and barley, the forecast for world total grains (wheat and coarse grains) production in 2025/26 is boosted by 8m t m/m (month-on-month), to 2,412m, up by 4% y/y (year-on-year). Despite unusually small carry-in stocks, the record crop will lift total supply above 3,000m t for the first time ever. The projection for total consumption is 4m t higher m/m, at 2,395m, mostly on an uprated feed estimate (wheat and maize). Taking into account larger than previously estimated opening stocks, the figure for world carryover inventories (aggregate of respective local marketing years) is raised by 9m t m/m, to 606m. Owing to projected stronger wheat import demand, the Council’s trade estimate is lifted for a second month in a row, to 438m t.

Tied to recent larger than anticipated shipments from South American origins, soyabean trade in 2024/25 (Oct/Sep) is forecast 2m t higher m/m. Owing to marginal adjustments, the 2025/26 world output projection is trimmed by 1m t m/m. With consumption seen near-unchanged from previously, carryovers are cut by 2m t. Expectations for trade are raised to a peak of 185m t (+2%).

The Council’s outlook for world rice production in 2025/26 is unchanged m/m but, due to elevated carry-in stocks, supplies are lifted from previously. Together with a marginal downgrading of consumption, this feeds through to a 3m t m/m increase in carryovers, pegged at an all-time high. Trade is projected steady m/m, at around 60m t (+2%).

The IGC Grains and Oilseeds Index (GOI) was little-changed compared to last month’s GMR, down by 4% y/y.

Total grains production is forecast to rise by 87m t in 2025/26, to an all-time high of 2,412m, with increases for all crops, barring rye. Uptake is also predicted to climb to a fresh record, up by 50m t, to 2,395m, including gains for food, feed and industrial uses. World stocks of grains are projected to expand by 17m t to 606m, still slightly short of the prior five-year average, including some increase in maize and barley inventories. Trade (Jul/Jun) in grains is expected to reach 438m t, up by 15m y/y and potentially the second highest on record.

Global soyabean production is forecast broadly steady y/y in 2025/26, at 429m t, as gains in South America compensate for falls elsewhere. Total use is seen advancing by 3% y/y as increased demand for soya derivatives across feed, food and industrial segments boosts processing to a peak. After the prior year’s solid gain, inventories could tighten, including in the three majors. Trade is predicted at a record on firmer Asian interest.

Building on the prior year’s gains, global rice supplies are seen at a fresh record in 2025/26, with the population trend expected to boost uptake to a new peak. Inventories are projected to build, with major exporters’ reserves seen at a high of 58m t, including 50m in India. Trade in 2026 is predicted to rise by 2% y/y, with India accounting for 40% of overall flows.

Global chickpeas output is projected to expand for a second consecutive year in 2025/26 as leading growers respond to growing local and international demand. With heavy outturns ensuring ample availabilities, aggregate end-season reserves are seen rising across the forecast period. After retreating slightly in the prior year, trade is seen edging up in 2026.

For almost 30 years of expertise in the agri markets, UkrAgroConsult has accumulated an extensive database, which became the basis of the platform AgriSupp.

It is a multi-functional online platform with market intelligence for grains and oilseeds that enables to get access to daily operational information on the Black Sea & Danube markets, analytical reports, historical data.

You are welcome to get a 7-day free demo access!!!

Read also

BLACK SEA GRAIN. KYIV: Join with a SMART rate by March 31!

China has opened its market to imports of Ukrainian peas

Vegetable oil prices have stopped responding to speculative jumps in cude oil prices

Thai sugar industry calls for E20 transition to bolster energy security

Trump considers suspending Moroccan fertilizers duties amid corn grower pressure

Got additional questions?

We will be happy to assist!

Write to us

Our manager will contact you soon