Global fertilizer market faces severe shock amid Iran war

The global fertilizer market is under significant pressure due to the military conflict in Iran and the associated geopolitical risks. Fertilizers account for 20–30% of operating costs for major crops worldwide, so any disruptions in prices or supply directly affect agricultural profitability.

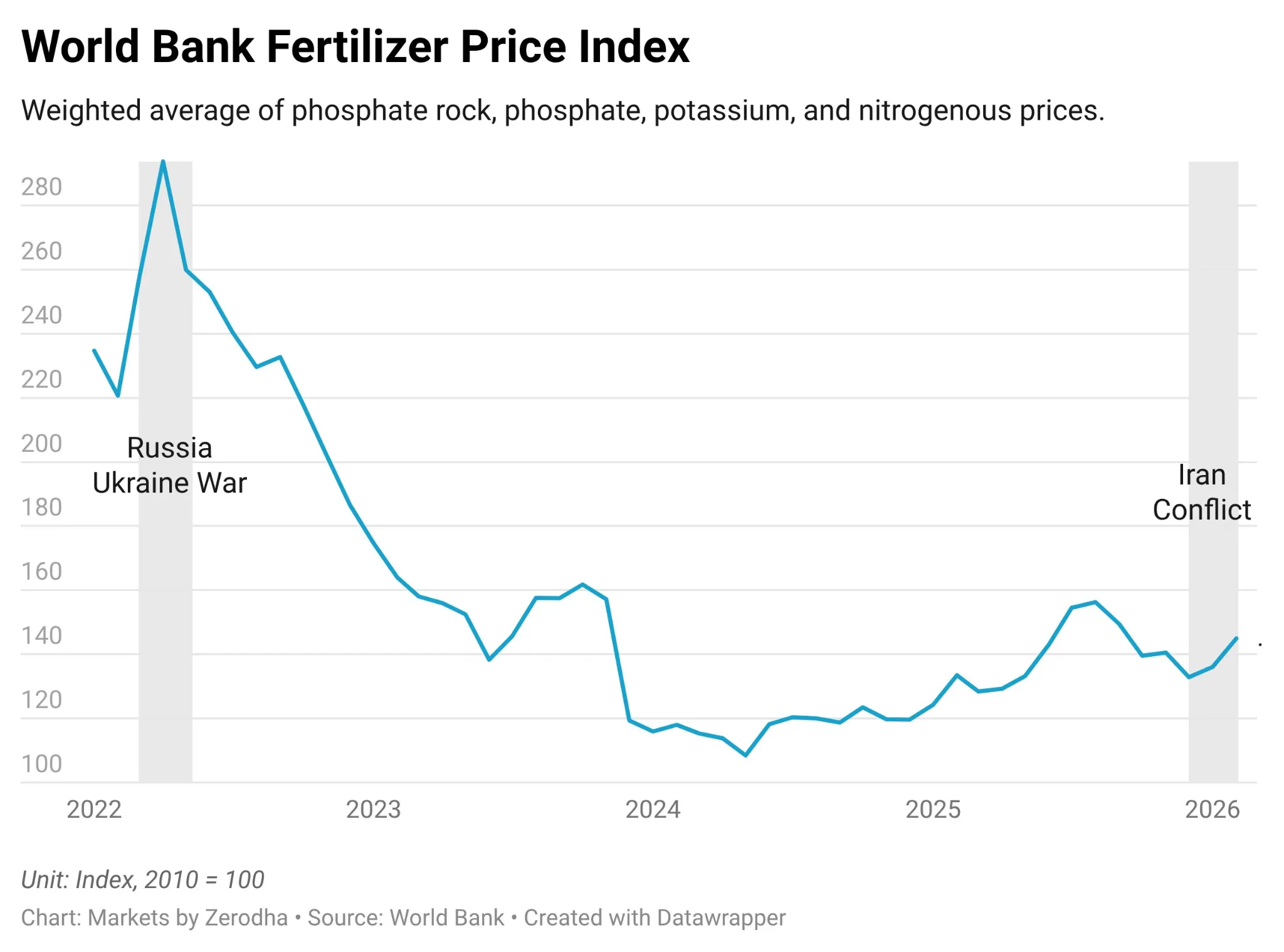

The war in Ukraine had already restructured global fertilizer trade, keeping prices at historically high levels and highlighting the risks of market concentration, where a few geopolitically unstable countries control large shares of essential resources for food production.

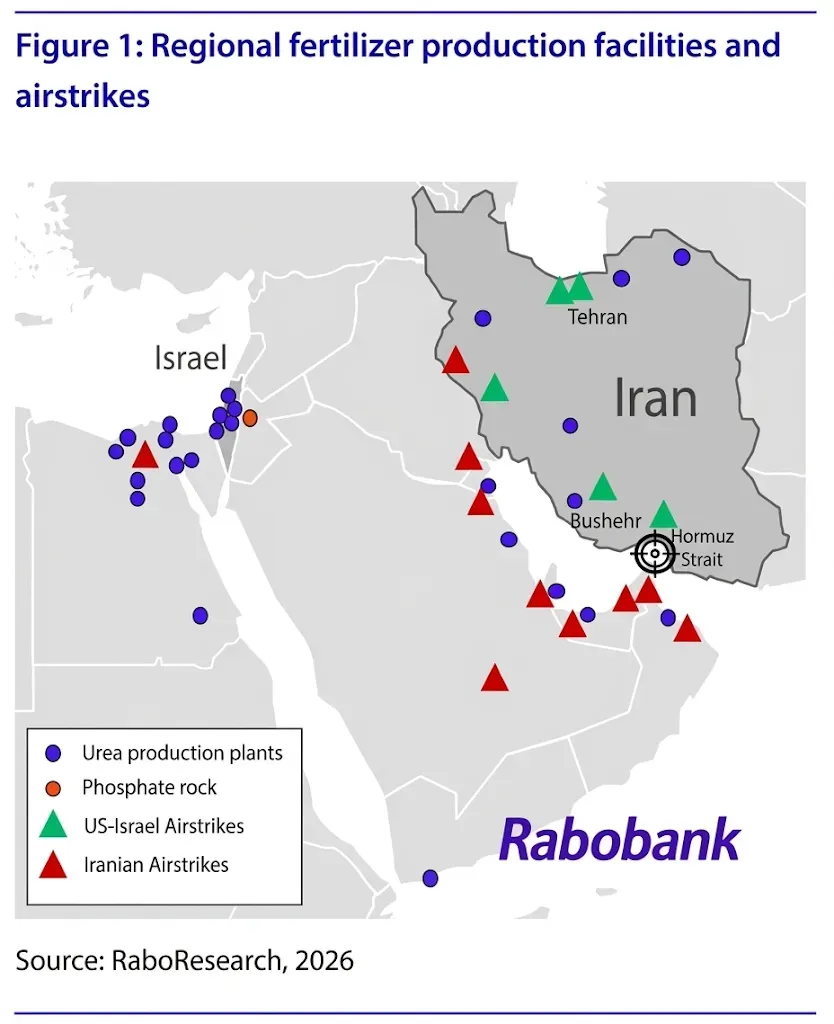

The new crisis intensified following the US-Israeli strikes on Iran starting February 28, 2026, and Iran’s subsequent closure of the Strait of Hormuz. This led to a sharp reduction in fertilizer shipments through the Persian Gulf, which handles roughly a third of global nitrogen fertilizer exports and significant shares of phosphate and sulfur fertilizers.

Within the first 48 hours after the strikes, North African urea prices surged nearly 20%, while EU natural gas (Dutch TTF) jumped 45%. By March 11, global urea benchmark prices rose from $465.5 to $585 per ton, reaching a three-year high. The Rabobank Urea Affordability Index fell to its second-lowest level since 2010, matching peak levels seen during the 2022 Russia-Ukraine war.

The disruption extends far beyond the Persian Gulf. Production and supply challenges are affecting Egypt, Algeria, Israel, and Jordan. Israel halted gas exports to Egypt, LNG facilities in the Gulf were damaged, Saudi refineries reduced runs, and North African producers faced operational constraints.

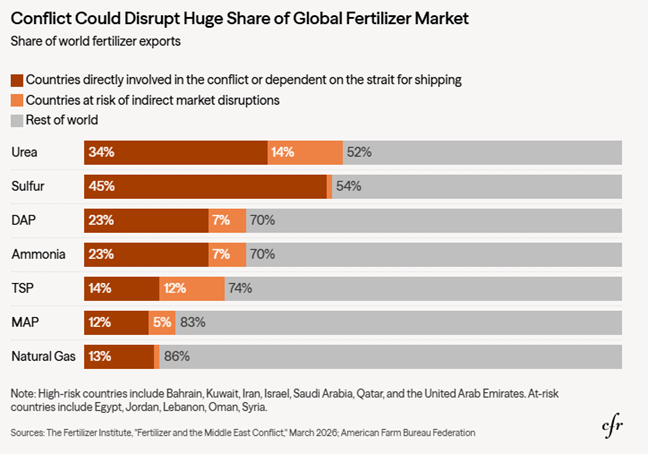

The global scale of risk is substantial: around 44% of global urea exports, 27% of ammonia, 25% of phosphate fertilizers, 47% of sulfur, and 36% of phosphate rock are at stake. The simultaneous impact on production and transportation creates a structurally vulnerable situation for the global agricultural sector.

The crisis affects not only nitrogen fertilizers but also phosphate and potash products due to rising ammonia and sulfur input costs. Ammonia prices have jumped 15–28%, and DAP is under additional pressure due to its strong correlation with ammonia. Some smaller phosphate plants in Brazil have already gone offline, with more potentially following.

For Europe, the Persian Gulf’s direct share of supply is small (1–2% of nitrogen and ammonia imports), but indirect effects are significant. Egypt and Algeria supply over 30% of Europe’s imported nitrogen and ammonia, both facing production disruptions and surging prices. European natural gas prices surged 45%, increasing manufacturing costs, and some plants had to temporarily suspend trading.

India, one of the world’s largest fertilizer consumers, is particularly exposed. About 60% of DAP and all imported potash come from the Gulf region. Petronet LNG declared force majeure, causing Indian fertilizer plants to halt or cut production. The government has implemented a priority gas allocation system for households, industrial users, and fertilizer plants.

Analysts warn that even if the conflict ends soon, restoring fertilizer production and transport could take weeks, coinciding with critical planting periods in the Northern Hemisphere. The global fertilizer market is currently under a double shock—disrupted production and transportation—with limited alternative suppliers, threatening farmer profitability and food security worldwide in 2026.

Got additional questions?

We will be happy to assist!

Write to us

Our manager will contact you soon